Facts and stupidity

The April Fool’s Day false news announcement is one of America’s most popular occasions for shameless publicity stunts. But if $ 69 million worth of Stonks, Dogecoin, and JPG files are real things worthy of serious business coverage, the risk of jokes being taken seriously could hardly be higher. Some say this is a good reason to skip them, not to mention the gravity a pandemic has thrown over things.

With that in mind, can you see the prank among these recent announcements? (Scroll down for the answer.)

A: To celebrate National Burrito Day today, Chipotle is giving away $ 100,000 worth of Bitcoin.

B: Volkwagen’s US business changes its name to “Voltwagen” to underline the company’s foray into electric vehicles.

C: Robinhood doesn’t do a confetti animation when app users complete a stock trade to reduce the “distraction”.

D: Krispy Kreme gives anyone who shows evidence of Covid-19 vaccination a free donut per day for the rest of the year.

E: Goldman Sachs managers are giving junior bankers gift baskets of fruit and snacks in response to complaints of burnout.

WHAT HAPPENS HERE

Corporate groups challenge President Biden’s proposed corporate tax hikes. The Business Roundtable and the US Chamber of Commerce praised Mr Biden’s plan to spend trillions on infrastructure, among others. But they rejected his idea of paying for it through tax hikes, saying it would jeopardize economic recovery.

The recent setbacks in fighting the pandemic. Johnson & Johnson said it would delay future deliveries of its vaccine after a mix-up at a manufacturing facility. A senior EU official said the bloc would allow “zero” shipments of AstraZeneca’s vaccine to the UK until the drugmaker honors its commitments to Brussels. And France announced a third nationwide lockdown as its cases surge and vaccination efforts lag.

A tough day for an IPO. With Deliveroo having “the worst IPO in London history,” other bids also struggled. In the US, SoftBank-backed real estate agent Compass was on the lower end of a reduced range, while budget airline Frontier sold on the lower end of expectations. And in Canada, space tech company MDA’s price was below its reach.

Microsoft wins a major contract to manufacture augmented reality headsets for the US Army. The tech giant will receive up to $ 22 billion to equip soldiers with sensors based on its HoloLens technology. It’s another big defense deal for Microsoft that Amazon beat Amazon to provide a $ 10 billion cloud computing system for the Pentagon.

Executives get a sense of urgency in Georgia

A day after 72 black executives signed a letter urging companies to fight more restrictive electoral laws, executives began to speak more directly about laws restricting access to ballot papers. However, their testimony came too late to sway a sweeping law passed in Georgia last week that added new postal voting requirements, dropboxing restrictions, and other restrictions that are having an over-the-top impact on black voters.

In business today

Updated

March 31, 2021, 6:27 p.m. ET

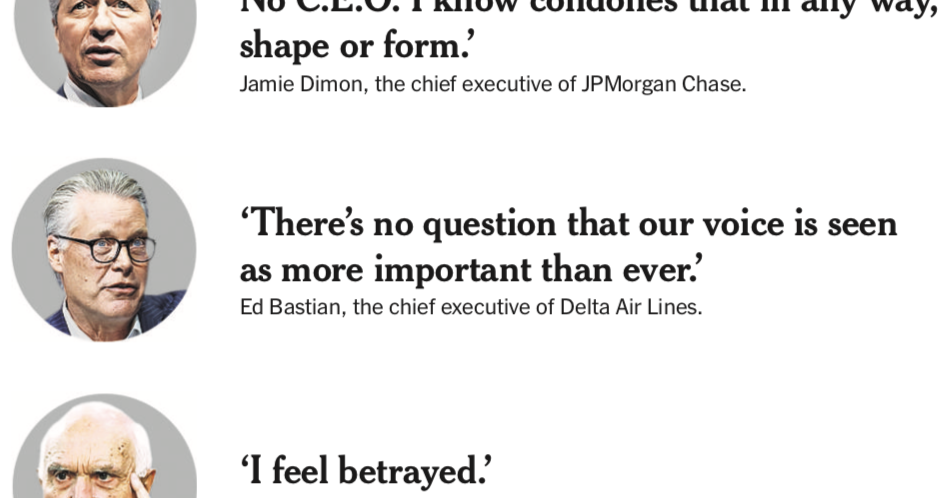

Delta and Coca-Cola reversed course. Ed Bastian, Delta CEO, told employees, “I need to make it clear that the final invoice is unacceptable and does not match Delta’s values.” James Quincey, CEO of Coca-Cola, said he wanted to be “crystal clear” that “The Coca-Cola Company does not support this legislation because it is harder for people to vote, not easier.”

-

The statements by Atlanta-based companies angered local politicians, including Governor Brian Kemp. In the past, corporate booths on controversial issues have led to political retaliation: In 2018, Lt. Gov. Casey Cagle passed a tax break proposal on a bill that would benefit Delta after the airline ended a promotional discount for NRA members. The State House passed a similar measure yesterday, but the Senate did not take it until the Houses were adjourned for the year.

-

Retaliatory measures also go in the other direction: In an interview with ESPN, President Biden said he would “strongly support” the move of the all-star game of Major League Baseball out of Atlanta in July.

“It is unfortunate that the sense of urgency came after the laws were passed and incorporated into the law.” said Darren Walker, the president of the Ford Foundation who is a board member at Pepsi, Ralph Lauren and Square.

Other Georgia-based companies remained cautious. A UPS spokesman said the company was “ready to continue to help ensure that every Georgian voter can vote”. A Home Depot spokesman reiterated the company’s stance that “all elections should be accessible, fair and safe”. A spokesman for Inspire Brands, the owner of Dunkin ‘Donuts and Arby’s, said it “values inclusivity” and that “every American should have equal access to voting rights.”

“The argument is that they are recruited, used up and then thrown aside without a college degree. So you are saying how can this be defended in the name of amateurism? “

– Judge Samuel Alito, who rated the “stark picture” college athletes painted in an antitrust case against the NCAA that the Supreme Court heard yesterday.

The Red Sox sold a stake in private equity. What now?

RedBird Capital Partners confirmed its agreement to purchase a stake in Red Sox parent Fenway Sports Group, a transaction valued at $ 7.35 billion. DealBook spoke to RedBirds founder Gerry Cardinale and Fenway’s chair Tom Werner about what’s next.

Buy and build. RedBird Plans to Add More Teams: Mr. Cardinale noted that his company has no teams in the NBA, NHL, or MLS. For its part, Fenway plans to open up new opportunities in the areas of ticketing, sponsorship and media. (As part of the RedBird deal, NBA star LeBron James bought a stake in Fenway.) In the media, Fenway controls NESN, and RedBird has a stake in the YES network. “You should expect that we will continue to seek innovation in this area,” said Cardinale, who helped build the YES network.

-

A deepening of relationships with online gambling is also on the table. “We have an excellent relationship with DraftKings,” said Werner, “and we have had several discussions with them about partnerships.”

The deal was better suited to the private market than a SPAC. Executives said after talks to bring Fenway to the public through a blank check company failed. “In the middle of Covid, with a mandate to redraw the next wave of growth for Fenway Sports Group, it would probably be better to do so privately and then give us the option,” Cardinale told Public. He also called the current SPAC market “very frothy”.

What worked at WeWork?

Founded in 2008, WeWork rose spectacularly, hitting a valuation of $ 47 billion, and known to crash ahead of a planned IPO in 2019. (It was announced last week that it would go public by partnering with a blank check company valued at roughly $ 8 billion.) A new documentary, “WeWork: Or the Make and Break of a $ 47 billion unicorn, “seeks to learn from the ups and downs. It’s streaming on Hulu starting tomorrow.

Jed Rothstein, the director, told DealBook that he believes what is most compelling about WeWork isn’t what went wrong, but how it initially managed to turn strangers into some sort of tribe. “We still need that,” he said.

“WeWork’s core idea met a real need for community.” Mr. Rothstein said. “The gaps that people were trying to fill just got more real.” After a year of social distancing, he likes the idea of curated common spaces that WeWork offered. Speaking to early WeWorkers who bought the Vision and later felt cheated, he was amazed at how much the company gave to its followers, especially the feeling of being part of something bigger. This is worth recognition in a world where people are increasingly remote in their careers and work for many different companies, Rothstein said.

WeWork co-founders Adam Neumann and Miguel McKelvey both shared childhood experiences. Mr. Rothstein said he thought they sincerely wanted to repeat the good in group life and inspired people who had not seen this before. But Mr. Neumann also focused on what he didn’t like – and shared it equally – and emphasized the “Eat what you kill” mentality. Ultimately, his hunger turned the community dream into a nightmare for many.

-

After speaking to people who followed the original vision, the director changed his perspective. “The people in the film experienced real growth and fulfillment mixed with their anger,” he said. “I realized that the story is much more nuanced.”

READ THE SPEED

deals

-

The media conglomerate Endeavor went public for the second time and raised $ 1.8 billion to gain full control of the Ultimate Fighting Championship. It also added Elon Musk to its board of directors. (WSJ, CNBC)

-

Vice Media is reportedly in talks to go public through the merger with a SPAC. And the SEC issued two notices for companies looking to go public through SPAC. (The information, SEC)

-

Junior bankers aren’t the only ones feeling burned out. Young lawyers too. (Business insider)

Politics and politics

-

New York was the 15th state to legalize recreational marijuana. (NYT)

-

Efforts by aides to Governor Andrew Cuomo to hide the Covid-19 death toll in New York state coincided with his efforts to win a multi-million dollar book deal. (NYT)

-

Accidental disclosure by the IRS resulted in a $ 1 billion tax dispute with Bristol Myers Squibb. (NYT)

technology

The best of the rest

-

The German advertising agency doubles the referral bonus for black applicants. (Insider)

-

Amazon wants most of its employees to be back in its offices, while the Carlyle Group and IBM prefer hybrid work models. (Insider, Bloomberg)

-

Paul Simon is the newest musician to sell his entire back catalog: Sony Music Publishing will purchase the collection, including classics like Bridge Over Troubled Water, for an undisclosed amount. (NYT)

Do you feel burned out? As more and more employees are thinking about returning to the office, our colleague Sarah Lyall writes about anxiety and exhaustion in late pandemics. Tell her how you are.

Answer to the April Fool’s joke quiz: B. If you are fooled by the Volkswagen prank, you are in good company. Volkswagen reportedly told journalists that drafting the announcement was no ploy. It later just called the stunt “a bit of fun”.